Gold investment terminology explained for institutional investors

- Shannon B

- Mar 20

- 9 min read

Many institutional investors and financial professionals struggle with the specialized terminology used in gold markets, leading to costly misunderstandings in trading decisions and portfolio management. Terms like allocated versus unallocated gold, LBMA Good Delivery standards, and contango can seem opaque without clear context. This guide clarifies essential gold investment terminology, providing you with the precise definitions and practical insights needed to enhance your trading strategies and make informed decisions. By mastering these terms, you’ll navigate gold markets with greater confidence and precision, improving both execution quality and risk management outcomes.

Table of Contents

Understanding standard gold bar specifications for institutional trading

Allocated versus unallocated gold: ownership and risk distinctions

Key gold price components and derivative instruments used by professionals

Gold’s role in portfolio risk management: hedging, safe-haven, and diversification nuances

Explore Galami Gold’s trusted solutions for professional gold investment

Key Takeaways

Point | Details |

Good Delivery specs | LBMA Good Delivery bars provide standardized weight, fineness, dimensions, and markings to ensure liquidity and acceptance in institutional trading. |

Allocated vs unallocated ownership | Allocating gold assigns specific bars to an owner with lower counterparty risk, while unallocated gold represents a general claim against the custodian’s inventory with higher risk. |

Allocated lowers settlement risk | Institutions typically prefer allocated arrangements for physical settlement and long term holdings to reduce settlement uncertainties. |

Bar markings ensure authenticity | Serial numbers refiner stamps fineness marks and year provide traceability to verify a bar’s identity during settlement and custody transfers. |

Understanding standard gold bar specifications for institutional trading

Institutional gold trading relies on standardized physical specifications that ensure liquidity, authenticity, and global acceptance. The LBMA Good Delivery bars represent the industry benchmark, establishing precise requirements that facilitate seamless transactions across international markets. These standards eliminate ambiguity and create a common language for professional traders worldwide.

LBMA Good Delivery bars specify weight, fineness, dimensions, and markings for institutional gold trading. Each bar must weigh between 350 and 430 fine troy ounces, with the typical bar containing approximately 400 troy ounces or 12.4 kilograms. The minimum fineness requirement stands at 995 parts per thousand, meaning the gold content must be at least 99.5% pure.

Physical dimensions matter for storage and handling efficiency. Good Delivery bars typically measure between 210 and 290 millimeters in length, 55 to 85 millimeters in width, and 25 to 45 millimeters in height. These specifications accommodate standardized vault storage systems used by custodians globally.

Mandatory markings ensure traceability and authenticity:

Serial number unique to each bar for tracking and verification

Refiner’s stamp identifying the accredited manufacturer

Fineness marking showing exact gold purity

Year of manufacture for historical record keeping

These markings serve as the bar’s identity documents, enabling rapid verification during settlement and custody transfers. Understanding gold trading standards institutional investors use prevents costly settlement delays and ensures compliance with exchange requirements.

Standard specifications comparison:

Specification | Requirement | Purpose |

Weight range | 350-430 fine troy ounces | Standardization for trading and storage |

Minimum fineness | 995 parts per thousand | Quality assurance and value consistency |

Length | 210-290 mm | Vault compatibility |

Required markings | Serial, refiner, fineness, year | Authentication and traceability |

Pro Tip: Always verify that your gold holdings meet Good Delivery standards before entering into institutional transactions, as non-conforming bars require costly remelting and recertification processes that can delay settlements by weeks.

Allocated versus unallocated gold: ownership and risk distinctions

The distinction between allocated and unallocated gold fundamentally shapes your ownership rights, cost structure, and risk exposure in institutional gold investments. This choice directly impacts how you manage counterparty risk and operational efficiency in your portfolio.

Allocated gold assigns specific physical bars to an owner with lower counterparty risk, while unallocated gold represents a claim on pooled gold with higher counterparty risk. In allocated arrangements, you own identified bars with unique serial numbers stored separately in your name. The custodian cannot lend, lease, or encumber your specific bars without explicit permission.

Unallocated gold provides a more cost-effective approach where you hold a general claim against the custodian’s gold inventory without ownership of specific bars. The custodian maintains a pool of gold backing multiple clients’ claims, similar to fractional reserve banking principles. This structure reduces storage and insurance costs significantly but introduces counterparty credit risk.

Institutions typically choose allocated gold for long-term strategic holdings and physical settlement requirements in physical gold allocation strategies. Unallocated accounts suit short-term trading, forwards, and over-the-counter transactions where cost efficiency outweighs ownership certainty. Many professional traders maintain both account types, using each for its optimal purpose.

Key distinctions include:

Allocated gold appears on your balance sheet as a tangible asset with full legal ownership

Unallocated gold represents a creditor claim against the custodian, making you an unsecured creditor in bankruptcy scenarios

Storage fees for allocated gold typically run 0.10% to 0.25% annually versus 0.02% to 0.05% for unallocated

Allocated gold eliminates fractional reserve exposure where custodians might hold insufficient physical gold to cover all claims

The risk differential becomes critical during financial stress when custodian solvency comes into question. Several bullion banks have faced scrutiny over their unallocated gold backing ratios, highlighting the importance of understanding your actual ownership position. Reviewing gold investment storage options helps align your storage choice with investment objectives and risk tolerance.

Pro Tip: For holdings exceeding 1,000 ounces or positions you plan to maintain beyond 12 months, allocated storage provides superior risk management despite higher costs, protecting you from custodian insolvency and operational failures.

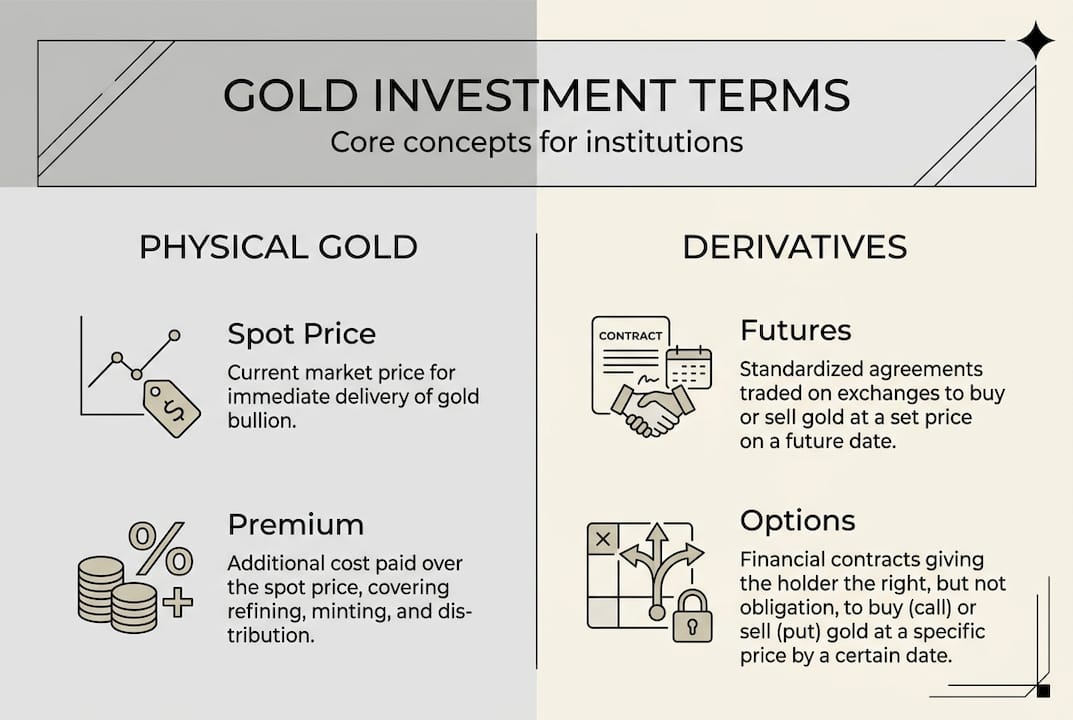

Key gold price components and derivative instruments used by professionals

Professional gold trading requires precise understanding of pricing components and derivative instruments that enable sophisticated hedging and speculation strategies. These tools form the foundation of institutional gold market participation and risk management.

The spot price is the real-time global gold price per troy ounce, representing immediate delivery value. It reflects continuous trading across global markets, with the London Bullion Market serving as the primary price discovery venue. Spot prices update constantly during trading hours, responding to supply, demand, currency movements, and macroeconomic developments.

Premium represents the additional cost above spot price when purchasing physical gold. Premium varies by product form, brand recognition, bar size, and market conditions. Institutional-sized Good Delivery bars typically carry premiums of 0.5% to 2% over spot, while smaller bars and coins command higher premiums due to fabrication costs and retail distribution expenses.

The bid-ask spread measures the difference between the price dealers pay to buy gold (bid) and the price they charge to sell (ask). Tight spreads indicate liquid markets with competitive pricing, while wide spreads signal illiquidity or elevated volatility. Institutional traders in major markets typically encounter spreads of $0.50 to $2.00 per ounce on spot transactions.

Derivative instruments enable precise risk management:

Instrument | Structure | Key Features |

Futures | Standardized exchange-traded contracts | Daily mark-to-market, margin requirements, high liquidity |

Forwards | Customized OTC agreements | Flexible terms, counterparty risk, settled at maturity |

Options | Rights without obligations | Premium payment, strike price selection, asymmetric risk profile |

Futures, forwards, and options offer different hedging methods with distinct cost and customization features. Futures contracts trade on exchanges like COMEX, providing standardized lot sizes (typically 100 troy ounces) and expiration dates. Daily settlement through variation margin ensures credit risk management but requires operational infrastructure for margin calls.

Forwards operate in over-the-counter markets, allowing customization of contract size, delivery date, and settlement terms. This flexibility suits corporate hedgers with specific exposure dates but introduces bilateral counterparty risk requiring credit assessment and collateral agreements.

Options grant the right, but not obligation, to buy (call) or sell (put) gold futures at predetermined strike prices. You pay an upfront premium for this optionality, creating asymmetric payoff profiles useful for directional views with defined risk. Options strategies range from simple protective puts to complex spreads balancing cost and protection levels.

Contango and backwardation describe the relationship between futures prices and spot prices:

Contango occurs when futures prices exceed spot prices, reflecting storage costs, insurance, and financing charges for holding physical gold

Backwardation happens when futures trade below spot, indicating immediate supply tightness or strong physical demand

The shape of the futures curve provides insights into market expectations and storage economics

Persistent backwardation often signals structural supply constraints or crisis-driven safe-haven demand

Understanding these components enables you to construct precise hedging strategies matching your risk exposures. Exploring gold market insights and gold trading advantages provides additional context for applying these instruments effectively in your portfolio management approach.

Gold’s role in portfolio risk management: hedging, safe-haven, and diversification nuances

Gold’s strategic value in institutional portfolios extends beyond simple diversification, encompassing distinct roles as hedge, safe-haven, and correlation reducer. Understanding these nuanced functions with empirical evidence allows you to deploy gold more effectively across different market environments and investment objectives.

Gold serves as a hedge with low or negative correlation to stocks and a safe-haven in several major markets during crises. Research demonstrates that gold exhibits zero or negative beta to equity markets in normal conditions, providing natural portfolio balance. This hedge characteristic stems from gold’s unique position outside traditional financial system dependencies and its inverse relationship with real interest rates.

During extreme market stress, gold functions as a safe-haven asset in major economies including Canada, Germany, Italy, the United Kingdom, and the United States. Safe-haven status means gold prices rise or remain stable when other assets decline sharply, providing liquidity and value preservation when you need it most. This behavior proved particularly valuable during the 2008 financial crisis and various geopolitical shocks.

However, gold may not always act as safe-haven during all crises, with variations in different countries and crisis types. The initial COVID-19 market shock in March 2020 saw gold decline alongside equities as investors liquidated positions for cash, demonstrating that safe-haven properties can temporarily weaken during extreme liquidity crises. This nuance matters when calibrating your expectations and position sizing.

Emerging markets often display stronger gold hedge effects due to cultural affinity, currency instability, and institutional factors. Countries with high gold ownership traditions and volatile domestic currencies see more pronounced safe-haven behavior, making geographic context essential for global portfolio construction.

Empirical portfolio benefits include:

Gold allocations of 5% to 10% historically reduced portfolio volatility by 0.5% to 1.5% annually while maintaining comparable returns

Negative correlation to the U.S. dollar provides natural currency hedge for dollar-denominated portfolios

Gold’s weak positive correlation to bonds (typically 0.1 to 0.3) offers diversification beyond traditional 60/40 stock-bond portfolios

During equity bear markets exceeding 20% drawdowns, gold generated positive returns in approximately 65% of historical episodes

“Gold’s diversification power comes not from its returns, but from its unique correlation structure that activates precisely when traditional asset class relationships break down during stress periods.”

Incorporating gold improves portfolio asset pricing models and lowers overall portfolio risk through correlation benefits that persist across multiple decades of data. The optimal allocation depends on your specific return objectives, risk tolerance, and views on monetary policy and geopolitical risks. Implementing effective portfolio risk management with gold requires understanding these conditional relationships rather than assuming static correlations.

Research on gold diversification benefits shows that strategic allocations consistently reduce portfolio drawdowns during crisis periods while adding minimal drag during bull markets. This asymmetric contribution to risk-adjusted returns makes gold valuable despite periods of underperformance relative to equities.

Pro Tip: Review country-specific and crisis-type gold behavior when designing global portfolio strategies, as safe-haven effectiveness varies significantly across regions and stress scenarios, requiring tailored allocation approaches rather than uniform rules.

Explore Galami Gold’s trusted solutions for professional gold investment

You’ve gained comprehensive understanding of gold investment terminology essential for institutional decision-making. Now apply this knowledge through proven platforms designed for professional traders and portfolio managers. Galami Gold provides audited physical gold trading solutions that align with the standards and practices detailed throughout this guide.

Our platform emphasizes disciplined execution, transparency, and risk management across established gold supply chains. Access high-return physical gold trading opportunities compliant with LBMA Good Delivery standards and institutional custody requirements. Whether you’re implementing allocated storage strategies, executing derivatives hedges, or optimizing portfolio diversification, Galami Gold delivers the infrastructure and expertise you need. Explore our gold investment strategy guide to translate terminology mastery into actionable portfolio improvements and trading strategies that enhance your risk-adjusted returns.

Frequently asked questions

What are LBMA Good Delivery bars in gold investment?

LBMA Good Delivery bars are gold bars meeting strict international standards for weight (350-430 fine troy ounces), purity (minimum 99.5% gold), and mandatory markings including serial numbers and refiner stamps. These specifications ensure global liquidity and trust in institutional gold trading by creating a standardized product recognized across all major markets.

How does allocated gold differ from unallocated gold?

Allocated gold means you own specific identified bars stored separately in your name, providing full legal ownership with minimal counterparty risk. Unallocated gold represents a general claim against a custodian’s pooled gold inventory, offering lower storage costs but higher counterparty risk since you’re an unsecured creditor without ownership of specific bars.

What is the significance of gold derivatives like futures and options?

Gold futures and options enable institutional investors to hedge price risk or speculate on gold movements without physical delivery requirements. Futures are standardized exchange-traded contracts with daily mark-to-market settlement, while options provide the right but not obligation to trade at predetermined prices, creating flexible risk management strategies with defined cost structures.

Is gold always a safe-haven asset?

Gold generally functions as a safe-haven in major economies like the U.S., U.K., Germany, and Canada during market stress, but its effectiveness varies by crisis type and geography. During extreme liquidity events like the initial COVID-19 shock, gold’s safe-haven properties can temporarily weaken as investors liquidate all assets for cash, making context-dependent analysis essential for portfolio planning.

How do contango and backwardation affect gold trading strategies?

Contango occurs when gold futures prices exceed spot prices, reflecting storage and financing costs, creating opportunities for cash-and-carry arbitrage strategies. Backwardation happens when futures trade below spot due to supply tightness or strong physical demand, often signaling crisis conditions and favoring strategies that benefit from immediate delivery premiums over deferred positions.

Recommended

Comments